Blank Idaho St 104 Mv PDF Form

Blank Idaho St 104 Mv PDF Form

| Fact Name | Description |

|---|---|

| Purpose | The ST-104-MV form is a Sales Tax Exemption Certificate for vehicles and vessels in Idaho. |

| Eligibility | This form is intended for nonresidents purchasing vehicles or vessels to use outside of Idaho. |

| Exemption Criteria | To qualify, the buyer must limit the vehicle's use in Idaho to 90 days or less within a 12-month period. |

| Submission Requirements | The completed form must be given to the seller, who then sends it to the Idaho State Tax Commission. |

| Governing Law | This form is governed by Idaho Code Section 63-3622R and Sales Tax Rule 101 & 107. |

| Prohibited Sales | Truck campers, canoes, paddleboards, and similar watercraft sold without a motor do not qualify for this exemption. |

Idaho State Tax Forms 2022 - Utilize available resources for assistance with the filing process.

In California, when you need to transfer ownership of a trailer, it's crucial to utilize the Trailer Bill of Sale form properly to avoid any ambiguities; for templates and resources, you can refer to fastpdftemplates.com/, which provides essential tools for ensuring a smooth transaction.

W9 Form 2022 - This form is required for payments made by the State of Idaho that may be reported to the IRS.

Small Claims Court Idaho - Proper records of any prior payment attempts should be attached as receipts.

Filling out the Idaho ST-104 MV form can be straightforward, but several common mistakes can complicate the process. One frequent error is failing to provide complete information. Every section of the form must be filled out accurately, including the buyer's and seller's names, addresses, and contact details. Incomplete forms may lead to delays or rejection of the exemption claim.

Another mistake involves misidentifying the vehicle type. The form requires specific selections, such as whether the vehicle is a truck, trailer, or vessel. Choosing the wrong category can invalidate the exemption. Buyers should double-check that they select the correct vehicle type based on the options provided.

Many people overlook the residency requirement. To qualify for the exemption, the buyer must not be an Idaho resident and must limit the vehicle's use in Idaho to 90 days or less within a year. Misunderstanding this condition can lead to complications, especially for those who may have recently moved to Idaho.

Additionally, some buyers fail to specify where they will take the vehicle. The form asks for the state or country where the vehicle will be licensed and titled. Omitting this information can cause issues later, as it is a crucial part of the exemption criteria.

Another common oversight is not providing a valid driver's license number or Employer Identification Number (EIN). This information is essential for verifying the buyer's identity and eligibility for the exemption. Ensure that this section is filled out completely and accurately.

Buyers sometimes forget to sign the form. A signature is not just a formality; it certifies that all information is true and correct. Without a signature, the form may be considered incomplete, leading to potential penalties.

Many individuals also fail to keep a copy of the completed form. It is important for both the buyer and seller to retain a copy for their records. This can be crucial if any questions arise regarding the exemption in the future.

Some people misinterpret the terms of the exemption. For example, the exemption does not apply to certain vehicles like truck campers and inflatable boats. Buyers should familiarize themselves with the list of ineligible items to avoid disappointment.

Lastly, buyers often neglect to submit the form to the appropriate authorities. After completing the ST-104 MV, it must be sent to the Idaho State Tax Commission or provided to the County Assessor when titling or registering the vehicle. Not following this step can result in unnecessary complications.

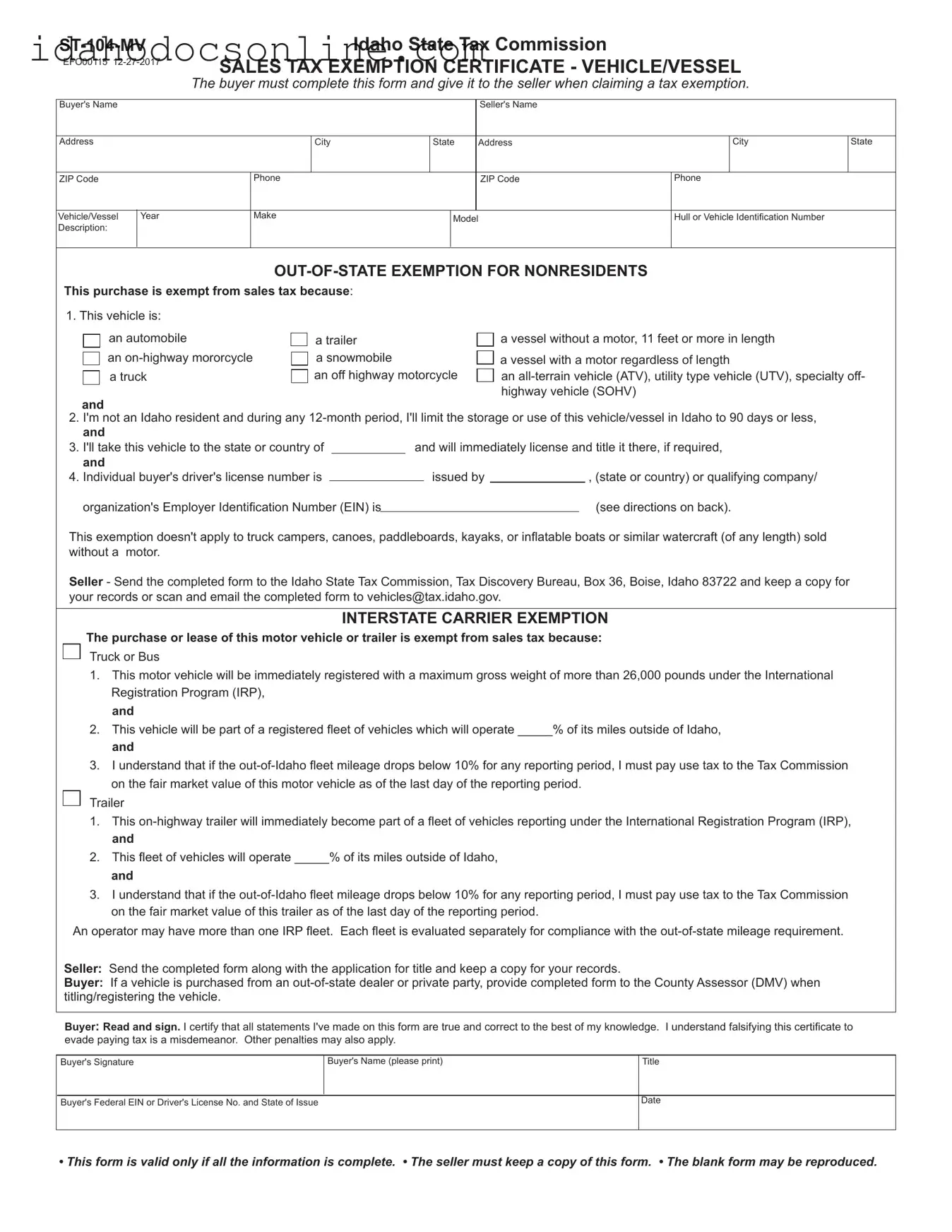

The Idaho ST-104-MV form serves as a Sales Tax Exemption Certificate for vehicles and vessels. Buyers use this form to claim an exemption from Idaho sales tax when purchasing a vehicle or vessel that will be used outside of Idaho. The completed form must be provided to the seller at the time of purchase.

Eligibility for using the ST-104-MV form is primarily for nonresidents who purchase a vehicle or vessel for use outside Idaho. To qualify, buyers must confirm that they will limit the storage or use of the vehicle or vessel in Idaho to 90 days or less within any 12-month period. Additionally, businesses must meet specific criteria to qualify for this exemption.

The exemption applies to various vehicles and vessels, including automobiles, trailers, vessels over 11 feet in length, motorcycles, snowmobiles, trucks, all-terrain vehicles (ATVs), and utility-type vehicles (UTVs). However, truck campers, canoes, paddleboards, kayaks, and inflatable boats do not qualify for the exemption.

Buyers need to complete several key pieces of information on the form, including their name, address, and driver's license number (or Employer Identification Number if applicable). They must also provide details about the vehicle or vessel, such as its year, make, model, and identification number. Additionally, buyers must certify that all statements made on the form are accurate.

Once the seller receives the completed ST-104-MV form, they must send it to the Idaho State Tax Commission, specifically to the Tax Discovery Bureau. It is crucial for sellers to keep a copy of the form for their records. They may also choose to scan and email the completed form to the Tax Commission.

Providing false information on the ST-104-MV form is considered a misdemeanor. Individuals may face legal consequences, including fines or other penalties, if they are found to have intentionally misrepresented information to evade paying sales tax.

The Interstate Carrier Exemption applies to motor vehicles and trailers used in interstate commerce. To qualify, the vehicle must be registered under the International Registration Plan (IRP) with a gross weight exceeding 26,000 pounds. Additionally, at least 10% of the vehicle's total fleet mileage must occur outside Idaho. Buyers must complete the ST-104-MV form and acknowledge that if their out-of-Idaho fleet mileage drops below the required percentage, they will owe use tax on the vehicle's fair market value.

When filling out the Idaho ST-104 MV form, it is important to follow specific guidelines to ensure the process goes smoothly. Here are four things you should do and four things you should avoid:

When navigating the process of vehicle or vessel purchases in Idaho, several forms and documents often accompany the Idaho ST-104 MV form. Each of these documents serves a specific purpose, ensuring compliance with state regulations and facilitating a smooth transaction. Here’s a brief overview of some commonly used forms:

Understanding these forms and documents can significantly ease the process of buying or selling a vehicle or vessel in Idaho. Each piece of paperwork plays a vital role in ensuring that the transaction is legally sound and that all parties are protected. Being well-informed about these requirements will help you navigate the process with confidence.

Completing the Idaho ST-104 MV form is an essential step for buyers claiming a sales tax exemption on vehicle or vessel purchases. After filling out the form, the buyer must provide it to the seller, who will then send it to the Idaho State Tax Commission. This process ensures that the necessary documentation is in place for the exemption to be valid.

Once the form is completed, the seller is responsible for sending it to the Idaho State Tax Commission. The buyer should keep a copy for their records. If the vehicle is purchased from an out-of-state dealer or private party, the buyer must provide the completed form to the County Assessor when titling or registering the vehicle.

|

|

|

|

|

Idaho State Tax Commission |

|

||||||||||||||

EFO00115 |

SALES TAX EXEMPTION CERTIFICATE - VEHICLE/VESSEL |

|

||||||||||||||||||

|

|

|

|

|||||||||||||||||

|

|

|

The buyer must complete this form and give it to the seller when claiming a tax exemption. |

|

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Buyer's Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

Seller's Name |

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Address |

|

|

|

|

|

City |

|

|

State |

Address |

|

|

City |

State |

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

ZIP Code |

|

|

|

|

Phone |

|

|

|

|

ZIP Code |

|

Phone |

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Vehicle/Vessel |

|

Year |

|

|

Make |

|

|

|

Model |

|

Hull or Vehicle Identification Number |

|

||||||||

Description: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|||||||||||||||

This purchase is exempt from sales tax because: |

|

|

|

|

|

|

|

|

|

|

|

|||||||||

1. This vehicle is: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

an automobile |

|

|

|

a trailer |

|

|

|

|

|

a vessel without a motor, 11 feet or more in length |

|

|||||||||

an |

|

a snowmobile |

|

|

|

|

|

a vessel with a motor regardless of length |

|

|||||||||||

a truck |

|

|

|

an off highway motorcycle |

|

an |

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

highway vehicle (SOHV) |

|

||||

and |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2. I'm not an Idaho resident and during any |

|

|||||||||||||||||||

and |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3. I'll take this vehicle to the state or country of |

and will immediately license and title it there, if required, |

|

||||||||||||||||||

and |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

4. Individual buyer's driver's license number is |

|

|

|

|

issued by |

, (state or country) or qualifying company/ |

|

|||||||||||||

organization's Employer Identifi cation Number (EIN) is |

|

|

|

|

|

|

|

|

(see directions on back). |

|

||||||||||

This exemption doesn't apply to truck campers, canoes, paddleboards, kayaks, or infl atable boats or similar watercraft (of any length) sold |

|

|||||||||||||||||||

without a |

motor. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Seller - Send the completed form to the Idaho State Tax Commission, Tax Discovery Bureau, Box 36, Boise, Idaho 83722 and keep a copy for your records or scan and email the completed form to vehicles@tax.idaho.gov.

INTERSTATE CARRIER EXEMPTION

The purchase or lease of this motor vehicle or trailer is exempt from sales tax because:

Truck or Bus

1.This motor vehicle will be immediately registered with a maximum gross weight of more than 26,000 pounds under the International Registration Program (IRP),

and

2.This vehicle will be part of a registered fl eet of vehicles which will operate _____% of its miles outside of Idaho, and

3.I understand that if the

Trailer

1.This

2.This fl eet of vehicles will operate _____% of its miles outside of Idaho, and

3.I understand that if the

An operator may have more than one IRP fl eet. Each fl eet is evaluated separately for compliance with the

Seller: Send the completed form along with the application for title and keep a copy for your records.

Buyer: If a vehicle is purchased from an

Buyer: Read and sign. I certify that all statements I've made on this form are true and correct to the best of my knowledge. I understand falsifying this certificate to evade paying tax is a misdemeanor. Other penalties may also apply.

Buyer's Signature

Buyer's Name (please print)

Title

Buyer's Federal EIN or Driver's License No. and State of Issue

Date

• This form is valid only if all the information is complete. • The seller must keep a copy of this form. • The blank form may be reproduced.

Instructions for Form

(Idaho Code Section

When a vehicle or vessel is bought by a nonresident for use outside Idaho, it may qualify for an exemption from Idaho sales tax. Truck campers, canoes, paddleboards, kayaks, infl atable boats, or similar watercraft (of any length) sold without a motor don't qualify for this exemption.

To claim an exemption the buyer must complete a Form

•Will immediately be taken out of Idaho and titled and registered in another state or country (if required), and

•Won't be stored or used in Idaho for more than 90 days in any

Idaho residents can't claim this exemption.

A company/organization qualifi es for this exemption only if it meets all three of the following criteria:

•It's a corporation, partnership, limited liability company, or other organization that isn't formed under the laws of Idaho,

and

•It's not required to be registered with the Idaho Secretary of State to do business in Idaho,

and

•It doesn't have signifi cant contacts and consistent operations in Idaho.

INTERSTATE CARRIER EXEMPTION

Sales of motor vehicles for use in interstate commerce are exempt if:

•The vehicle will be immediately registered with a maximum gross registered weight of more than 26,000 pounds under the International Registration Plan,

and

•At least 10% of the purchaser's total fl eet mileage is outside of Idaho.

The buyer must complete Form

The exemption applies only to purchases of trucks, buses, and trailers, but not their repair or maintenance. However, the sale of a "glider kit" isn't taxable when used to assemble a glider kit vehicle that will be registered in an IRP fl eet and will meet the weight and mileage requirements listed above.

Rule 128 states that if you don't receive an exemption certifi cate from the buyer at the time of sale, the sale is presumed to be taxable. If you receive an exemption certifi cate after the sale, but don't get it within a reasonable length of time, the Tax Commission will review the certifi cate with all other avail- able evidence to determine whether you have clearly proven that the sale was exempt from tax.

EFO00115

Misconceptions about the Idaho St 104 MV form can lead to confusion and mistakes. Here are six common misconceptions explained: