Blank Idaho 75 PDF Form

Blank Idaho 75 PDF Form

| Fact Name | Detail |

|---|---|

| Purpose | The Idaho 75 form is used to claim refunds for Idaho fuels tax paid on gasoline and special fuels used for nontaxable purposes. |

| Eligibility | Any individual or entity that purchases 50 gallons or more of Idaho tax-paid gasoline or any amount of special fuels may file for a refund. |

| Filing Period | The form must be completed for fuel purchased on or after July 1, 2008. |

| Governing Law | The Idaho Code Title 63, Chapter 24 governs the Idaho fuels tax and the refund process. |

| Non-Taxable Uses | Fuel used in unregistered equipment, stationary engines, or for home heating qualifies for a refund. |

| Signature Requirement | The form must be signed to be valid. An unsigned form will delay processing of any refund. |

W9 Form 2022 - Accuracy in account details prevents payment issues with the state.

For those navigating healthcare decisions, understanding the role of a trusted Medical Power of Attorney advocate can be invaluable. This document empowers individuals to appoint someone who can communicate and enforce their medical preferences when they are unable to do so, ensuring their wishes are honored and upheld.

Idaho Amended Tax Return - Keeping abreast of changes to the form's requirements ensures proper compliance.

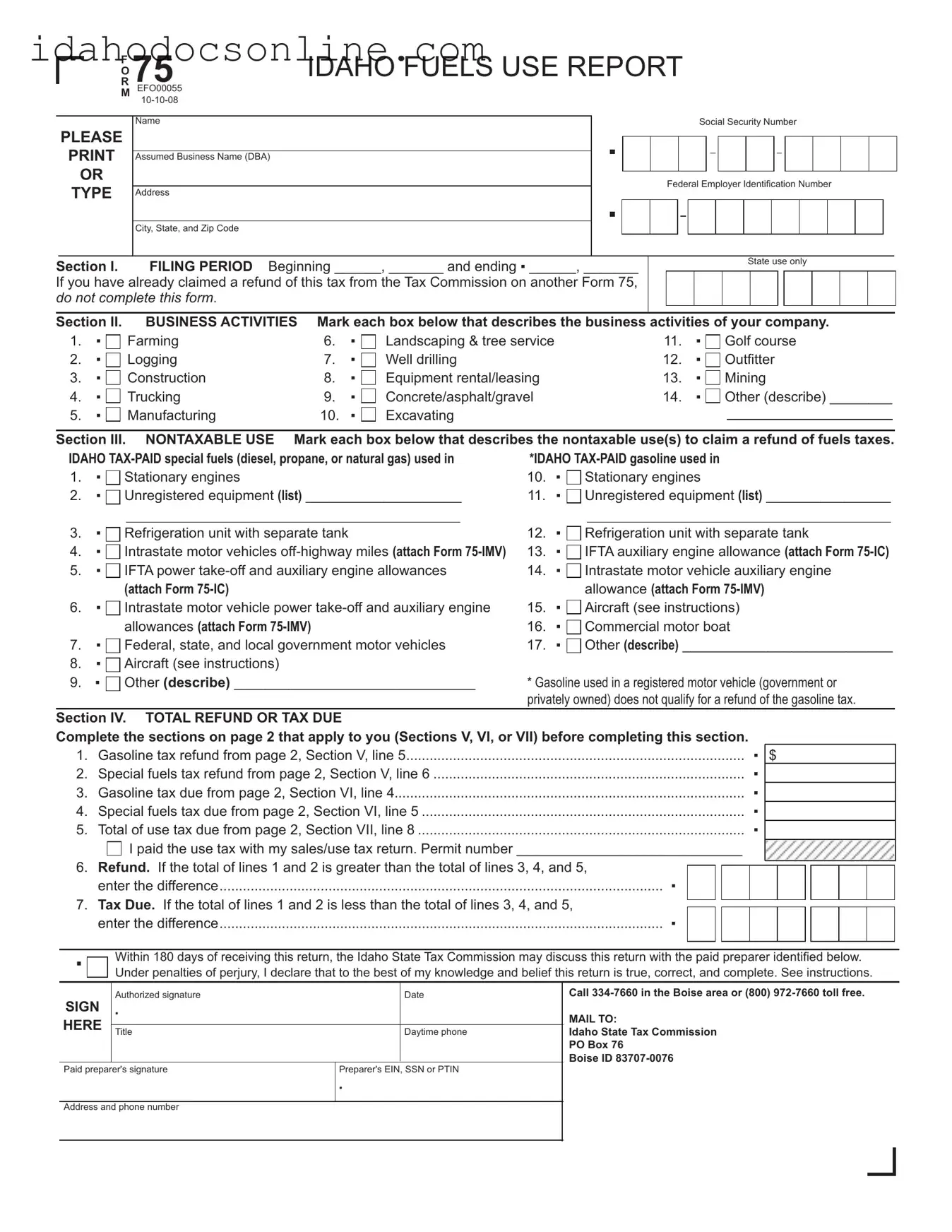

Filling out the Idaho 75 form can be a straightforward process, but many people make common mistakes that can lead to delays or even denials of their refund claims. One frequent error occurs in Section I, where individuals fail to enter the correct beginning and ending dates for the filing period. This section is critical, as it establishes the timeframe for which the refund is being requested. Omitting or incorrectly inputting these dates can result in the form being returned for correction.

Another common mistake is found in Section II, where business activities are specified. Some filers neglect to mark all applicable boxes that describe their business activities. This oversight can lead to incomplete information being provided, which may hinder the processing of the claim. It is essential to review the list carefully and ensure that every relevant activity is marked.

In Section III, which addresses nontaxable uses of fuel, filers often forget to provide additional details when they select "Other." If a unique nontaxable use is applicable, it must be clearly described in the space provided. Failing to do so can result in confusion and may ultimately affect the approval of the refund.

Moving to Section IV, many individuals miscalculate their total refund or tax due. This section requires careful addition and subtraction of various lines. A simple arithmetic error can lead to significant discrepancies in the amounts claimed. It is advisable to double-check all calculations before submission.

Another mistake occurs when individuals do not sign the form. An unsigned Idaho 75 form will be considered incomplete and can cause delays in processing. Filers should always ensure that they provide their signature, along with the date, in the designated area.

Moreover, some people mistakenly assume they can claim refunds for gasoline used in registered motor vehicles. This is not allowed, as the form clearly states that gasoline used in registered vehicles does not qualify for a refund. Ignoring this rule can lead to denied claims and wasted time.

Lastly, a frequent oversight involves recordkeeping. Many filers do not maintain the necessary documentation to support their claims. The Idaho State Tax Commission requires that records, such as receipts for tax-paid fuel purchases, be kept on file. Without this documentation, the right to a refund may be waived. It is crucial to keep thorough records to substantiate any claims made on the Idaho 75 form.

What is the Idaho 75 Form?

The Idaho 75 Form is a Fuels Use Report used to claim refunds for Idaho tax-paid fuels that were used for nontaxable purposes. This form is essential for individuals or businesses that have purchased fuels like gasoline, diesel, propane, or natural gas and wish to recover the tax paid on those fuels.

Who is eligible to file the Idaho 75 Form?

Any person or entity that has purchased 50 gallons or more of Idaho tax-paid gasoline or any amount of Idaho tax-paid special fuels can file this form. Only the final user of the fuel may submit the claim. Partnerships or corporations must report refunds or taxes due under the business name, while sole proprietorships can report under the individual's name.

What types of business activities can I report on this form?

You can mark various business activities on the form, including farming, logging, construction, trucking, manufacturing, and more. If your activity does not fit any listed categories, you can describe it in the “Other” section.

What qualifies as a nontaxable use of fuel?

Nontaxable uses include fuel used in stationary engines, unregistered equipment, refrigeration units, and for home heating. Additionally, fuel used in federal, state, or local government vehicles is also considered nontaxable. However, gasoline used in registered motor vehicles does not qualify.

How do I calculate my refund or tax due?

First, complete the relevant sections on page 2 of the form. Calculate the total gallons of fuel purchased and the gallons used for nontaxable purposes. Then, apply the appropriate tax rates to determine the refund amount or tax due. If your refund exceeds your tax due, you will enter the difference as a refund, otherwise, it will be reported as tax due.

What are the recordkeeping requirements?

You must keep detailed records to support your claim. This includes receipts for all tax-paid fuel purchased and documentation showing how much was used in both taxable and nontaxable applications. Failure to maintain these records may result in the denial of your refund claim.

Can I file the Idaho 75 Form with my income tax return?

Yes, you can file the Idaho 75 Form along with your income tax return. When doing so, report the refund or tax due amounts on the appropriate lines of your tax return. However, do not claim a refund for the same fuel on multiple forms.

What happens if I do not sign the form?

Failure to sign the Idaho 75 Form can delay your refund. It is crucial to provide an authorized signature to validate your submission. Unsigned forms may be returned for correction.

Where do I mail the completed Idaho 75 Form?

Send the completed form to the Idaho State Tax Commission at PO Box 76, Boise, ID 83707-0076. Ensure that you include all necessary information and signatures to avoid delays.

When filling out the Idaho 75 form, keep these important do's and don'ts in mind:

The Idaho 75 form is essential for claiming refunds on fuel taxes in Idaho. However, several other forms and documents are often used in conjunction with it. Here’s a brief overview of five key documents that may accompany the Idaho 75 form.

Using these forms and documents correctly will streamline the process of claiming refunds and ensure compliance with state regulations. Always keep thorough records to support your claims and consult with a professional if you have questions.

Completing the Idaho 75 form involves several steps to ensure accurate reporting of fuel use and potential refunds. It is essential to provide all required information and follow the instructions carefully to avoid delays or issues with your submission.

Once you have filled out the form, it is important to review all sections for completeness. Inaccuracies or omissions may lead to delays in processing your refund or tax due. After ensuring everything is correct, you can mail the completed form to the Idaho State Tax Commission at the address provided.

|

|

RO |

75 |

IDAHO FUELS USE REPORT |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

|

|

F |

EFO00055 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

M |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Social Security Number |

|||||||||||||||||||

|

|

|

|

|

Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||

|

PLEASE |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

Assumed Business Name (DBA) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

OR |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Federal Employer Identiication Number |

|||||||||||||||||||||||||

|

TyPE |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||

|

|

|

Address |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City, State, and Zip Code |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Section I. |

|

|

FILING PERIOD Beginning ______, _______ and ending ▪ ______, _______ |

|

|

|

|

|

|

|

|

|

|

|

State use only |

|||||||||||||||||||||||||||

If you have already claimed a refund of this tax from the Tax Commission on another Form 75, |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

do not complete this form. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Section II. |

|

|

BUSINESS ACTIVITIES Mark each box below that describes the business activities of your company. |

|||||||||||||||||||||||||||||||||||||||

1. |

▪ |

|

Farming |

6. |

▪ |

Landscaping & tree service |

|

11. |

|

|

▪ |

Golf course |

||||||||||||||||||||||||||||||

2. |

▪ |

|

Logging |

7. |

▪ |

Well drilling |

|

|

12. |

|

|

▪ |

Outitter |

|||||||||||||||||||||||||||||

3. |

▪ |

|

Construction |

8. |

▪ |

Equipment rental/leasing |

|

13. |

|

|

▪ |

Mining |

||||||||||||||||||||||||||||||

4. |

▪ |

|

Trucking |

9. |

▪ |

Concrete/asphalt/gravel |

|

14. |

|

|

▪ |

Other (describe) ________ |

||||||||||||||||||||||||||||||

5. |

▪ |

|

Manufacturing |

10. |

▪ |

Excavating |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

Section III. |

NONTAXABLE USE |

Mark each box below that describes the nontaxable use(s) to claim a refund of fuels taxes. |

||||||||||||||||||||||||||||||||||||||||

|

Idaho |

*Idaho |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||

1. |

▪ |

Stationary engines |

|

|

|

|

10. |

▪ |

Stationary engines |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

2. |

▪ |

Unregistered equipment (list) ____________________ |

11. |

▪ |

Unregistered equipment (list) ________________ |

|||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3. |

▪ |

Refrigeration unit with separate tank |

|

|

|

12. |

▪ |

Refrigeration unit with separate tank |

||||||||||||||||||||||||||||||||||

4. |

▪ |

Intrastate motor vehicles |

13. |

▪ |

IFTA auxiliary engine allowance (attach Form |

|||||||||||||||||||||||||||||||||||||

5. |

▪ |

IFTA power |

14. |

▪ |

Intrastate motor vehicle auxiliary engine |

|||||||||||||||||||||||||||||||||||||

|

|

|

(attach Form |

|

|

|

|

|

|

allowance (attach Form |

||||||||||||||||||||||||||||||||

6. |

▪ |

Intrastate motor vehicle power |

15. |

▪ |

Aircraft (see instructions) |

|||||||||||||||||||||||||||||||||||||

|

|

|

allowances (attach Form |

|

|

|

16. |

▪ |

Commercial motor boat |

|||||||||||||||||||||||||||||||||

7. |

▪ |

Federal, state, and local government motor vehicles |

17. |

▪ |

Other (describe) ___________________________ |

|||||||||||||||||||||||||||||||||||||

8.▪  Aircraft (see instructions)

Aircraft (see instructions)

9. ▪ |

Other (describe) _______________________________ |

* Gasoline used in a registered motor vehicle (government or |

|

|

privately owned) does not qualify for a refund of the gasoline tax. |

Section IV. TOTAL REFUND OR TAX DUE

Complete the sections on page 2 that apply to you (Sections V, VI, or VII) before completing this section.

1. |

Gasoline tax refund from page 2, Section V, line 5 |

|

|

|

▪ |

$ |

|

|

|

|

|

|

2. |

Special fuels tax refund from page 2, Section V, line 6 |

|

|

|

▪ |

|

|

|

|

|

|

|

3. |

Gasoline tax due from page 2, Section VI, line 4 |

|

|

|

▪ |

|

|

|

|

|

|

|

4. |

Special fuels tax due from page 2, Section VI, line 5 |

|

|

|

▪ |

|

|

|

|

|

|

|

5. |

....................................................................................Total of use tax due from page 2, Section VII, line 8 |

|

|

|

▪ |

|

|

|

|

|

|

|

|

I paid the use tax with my sales/use tax return. Permit number _____________________________ |

|

|

|

|

|

|

|||||

6. |

Refund. If the total of lines 1 and 2 is greater than the total of lines 3, 4, and 5, |

▪ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|||

|

enter the difference |

|

|

|

|

|

|

|

|

|

|

|

7. |

Tax Due. If the total of lines 1 and 2 is less than the total of lines 3, 4, and 5, |

▪ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|||

|

enter the difference |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

.

Within 180 days of receiving this return, the Idaho State Tax Commission may discuss this return with the paid preparer identiied below. Under penalties of perjury, I declare that to the best of my knowledge and belief this return is true, correct, and complete. See instructions.

|

Authorized signature |

|

Date |

SIGN |

▪ |

|

|

HERE |

|

|

|

Title |

|

Daytime phone |

|

|

|

|

|

Paid preparer's signature |

Preparer's EIN, SSN or PTIN |

||

|

|

▪ |

|

|

|

|

|

Address and phone number |

|

|

|

|

|

|

|

Call

MAIL TO:

Idaho State Tax Commission

PO Box 76

Boise ID

EFO00055 |

|

|

|

|

|

Form 75 Page 2 |

|||

|

|

|

A |

B** |

C** |

D |

E |

F |

G |

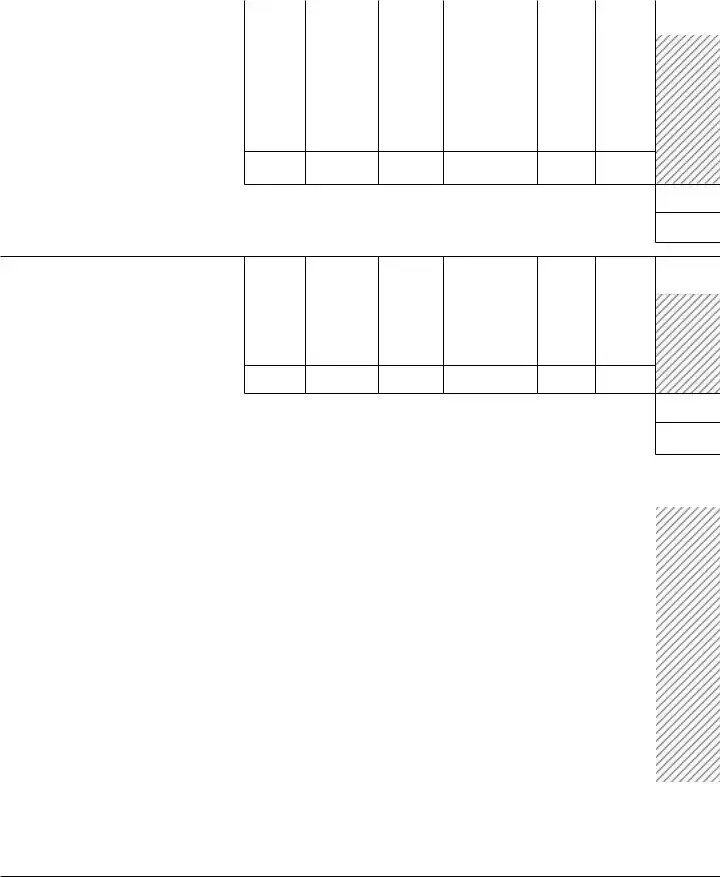

Section V. FUELS TAX REFUND |

|

Gasoline |

Av Gas |

Jet Fuel |

Undyed Diesel* |

Propane |

Nat Gas |

Totals |

|

|

|

|

|

|

|

|

|

|

|

1. |

Total |

|

|

|

|

|

|

|

|

|

from all sources (whole gallons) .... |

▪ |

|

|

|

|

|

|

|

2. |

Total nontaxable gallons |

|

|

|

|

|

|

|

|

|

(whole gallons) |

▪ |

|

|

|

|

|

|

|

3. |

Tax rate |

.25 |

.07 |

.06 |

.25 |

.181 |

.197 |

|

|

4.Fuels tax refund .............................

5.Gasoline tax refund. Add line 4, columns A, B & C. Enter here and on page 1, Section IV, line 1 ................................

6.Special fuels tax refund. Add line 4, columns D, E & F. Enter here and on page 1, Section IV, line 2 ..........................

|

|

|

A |

B** |

C** |

D |

E |

F |

G |

Section VI. FUELS TAX DUE |

|

Gasoline |

Av Gas |

Jet Fuel |

Undyed Diesel* |

Propane |

Nat Gas |

Totals |

|

|

|

|

|

|

|

|

|

|

|

1. |

Taxable gallons |

|

|

|

|

|

|

|

|

|

(whole gallons) |

▪ |

|

|

|

|

|

|

|

2. |

Tax rate |

.25 |

.07 |

.06 |

.25 |

.181 |

.197 |

|

|

3.Fuels tax due .................................

4.Gasoline tax due. Add line 3, columns A, B & C. Enter here and on page 1, Section IV, line 3 ..................................

5.Special fuels tax due. Add line 3, columns D, E & F. Enter here and on page 1, Section IV, line 4.............................

|

|

|

A |

B** |

C** |

D |

E |

F |

G |

|

Section VII. USE TAX DUE |

|

Gasoline |

Av Gas |

Jet Fuel |

Undyed Diesel* |

Propane |

Nat Gas |

Totals |

||

|

|

|

|

|

|

|

|

|

|

|

1. |

Number of gallons from |

|

|

|

|

|

|

|

|

|

|

Section V, line 2 |

▪ |

|

|

|

|

|

|

|

|

2. |

Average price per gallon |

|

|

|

|

|

|

|

|

|

|

(carry 4 decimal places x.xxxx) |

▪ |

|

|

|

|

|

|

|

|

3. |

Less state fuels tax/gallon |

|

|

|

|

|

|

|

|

|

4. |

Less federal fuels tax/gallon |

▪ |

|

|

|

|

|

|

|

|

5. |

The base cost per gallon |

|

|

|

|

|

|

|

|

|

|

(line 2 less 3 & 4) |

|

|

|

|

|

|

|

|

|

6. |

Total amount subject to use tax |

|

|

|

|

|

|

|

|

|

|

(multiply line 1 by line 5) |

|

|

|

|

|

|

|

|

|

7. |

Use tax due |

|

|

|

|

|

|

|

|

|

|

(multiply line 6 by 6%) |

|

|

|

|

|

|

|

|

|

8. |

Use tax due. Add line 7, columns A through F. Enter here and on page 1, Section IV, line 5 |

|

|

|

|

|||||

* Includes Biodiesel and Biodiesel Blends

** Rate change for Av Gas and Jet Fuel effective July 1, 2008.

EFO00055p3

Instructions for Idaho Form 75

Use this form for fuel purchased ON OR AFTER July 1, 2008.

WHO MAy FILE

Any person or entity that has purchased 50 gallons or more of Idaho

Only the inal user (consumer) of the fuel may ile Form 75.

•Any refund or tax due to a partnership or corporation must be reported by the business. It may not be applied to the individual returns iled by partners or shareholders.

•Any refund or tax due to a sole proprietorship must be reported by that individual.

You may claim a refund or report fuels tax due in one of the following ways: a) monthly, b) quarterly, c) annually, or

d)alternate period (any period greater than one month but not more than one year.)

If you ile the claim with your Idaho income tax return,

report the amount of the tax due or refund amount on the proper line of your income tax return, and attach a Form 75 to your return.

NOTE: Do not claim a refund for

claimed a refund for the same

You may claim a refund of Idaho fuels tax if:

•You buy fuel with Idaho fuels tax included and use the fuel for a nontaxable purpose. This includes using the fuel: in unregistered equipment; to operate a stationary engine; in a refrigeration unit or other auxiliary equipment that has a supply tank separate from the main supply tank of the motor vehicle; or for home heating purposes.

•You ile reports under the International Fuel Tax Agreement (IFTA) or operate an intrastate motor vehicle and use fuel from the main supply tank of a registered motor vehicle to operate power

•You operate an intrastate motor vehicle and use special fuels on nontaxable roads. You must complete and attach the Idaho Fuels Tax Refund Worksheet, Form

•You use special fuels in a motor vehicle owned and operated or leased and operated by an agency of the federal government or the state of Idaho, including its political subdivisions (local government).

•You buy gasoline or special fuels with Idaho motor fuels tax included and use the fuel in an aircraft. You may only claim a refund of the difference between the Idaho motor fuels tax rate and the aviation gasoline or jet fuel tax rate. See the section titled Aircraft Fuels Tax Refund.

you may not claim a refund of Idaho fuels tax for:

•Gasoline used in registered motor vehicles.

•Gasoline or special fuels used in recreational vehicles or noncommercial motorboats.

•Gasoline purchased from an

•Special fuels purchased from certain

You owe Idaho fuels tax if you purchased gasoline, special fuels, or aircraft fuel, and:

•You did not pay the Idaho fuels tax at the pump (including gasoline purchased from

•You used the fuel for a taxable purpose in Idaho.

*For information about

RECORDKEEPING REQUIREMENTS

You must keep records that support your fuels tax refund claim. These records include all motor fuels receipts showing the total gallons of

AIRCRAFT FUELS TAX REFUND

If you have paid the aviation gasoline tax or the jet fuel tax, no additional tax or refund is due.

Gasoline. If you buy gasoline and pay Idaho gasoline tax, then use the gasoline in an aircraft, you are entitled to a refund of the difference between the gasoline tax rate and the aviation gasoline tax rate.

Diesel. If you buy undyed diesel fuel and pay the Idaho diesel fuel tax, then use the

EFO00055p4

Instructions for Idaho Form 75 - page 2

aircraft, you are entitled to a refund of the difference between the diesel fuel tax rate and the jet fuel tax rate.

Complete Section V FUELS TAX REFUND to compute

the refund amount for the gasoline and/or diesel fuel tax

and Section VI FUELS TAX DUE to compute the aviation

gasoline and/or jet fuel tax due.

AIRCRAFT FUELS TAX DUE

Complete Section VI FUELS TAX DUE of this form to compute the aircraft fuels tax due if the Idaho fuels tax has not been paid on the diesel, gasoline, or other fuels used in your aircraft. You must report the tax due at the jet fuel or aviation gasoline tax rate.

USE TAX DUE

Use tax does not apply when the fuel purchased would qualify for the production, manufacturing,

farming, or other exemptions.

When fuel is not subject to motor fuels tax, it is subject to sales tax unless a sales tax exemption applies. If sales tax was not collected on its purchase, the purchaser owes use tax.

Use tax is a tax on goods that are put to use in Idaho. If sales tax has not been paid on goods that are used (or stored for later use), the person who uses or stores the goods in Idaho owes a use tax (unless the goods are held for resale or some other exemption applies).

The sale of motor fuel is exempt from sales and use tax if the fuel is subject to motor fuel tax or if the motor fuel tax is paid when the fuel is purchased. However, when a refund of the motor fuel tax is obtained, the value of the fuel less the state and federal taxes, if applicable, becomes subject to use tax. (See Speciic Line 4

Instructions for Section VII to determine if federal taxes are deductible.)

If you owe use tax, you must report it on your Idaho income tax return, Idaho sales or use tax return, or Form 75 by completing Section VII USE TAX DUE.

DETAILED INSTRUCTIONS

TAXPAyER INFORMATION

Enter name, assumed business name (DBA) (the name under which you are doing business), address, and Social Security number (SSN) or federal Employer Identiication Number (EIN).

If you are reporting as an individual or sole proprietor and

not as an S corporation, corporation, partnership, estate, or trust, you must use your SSN. DO NOT USE AN EIN.

yOU MUST PROVIDE THE INFORMATION REQUESTED FOR SECTIONS I, II, AND III TO RECEIVE A FUELS TAX REFUND. IF A FORM IS NOT COMPLETE, WE MAy RETURN IT TO yOU FOR CORRECTION.

FILING PERIOD

Section I. Enter the appropriate beginning and ending date for the iling period.

BUSINESS ACTIVITIES

Section II. Mark each box that describes the business activities of your company. If your company’s business activities are not described by any of the listed categories, mark the “Other” box and describe your company’s business activities.

NONTAXABLE USE

Section III. Mark each box that describes the nontaxable use(s) to claim a refund of fuels taxes. For unregistered equipment, list the type of equipment in the space next to the boxes. Attach additional pages if needed. If you have nontaxable use of fuel that is not described by any of the listed categories, mark the “Other” box and describe your nontaxable use.

ROUNDING AMOUNTS

Except for lines 2, 3, 4, and 5 of Section VII, round the amounts on this report to the whole gallon or dollar. Reduce amounts less than .50 to the whole gallon or dollar. Increase amounts of .50 or more to the next whole gallon or dollar.

FUELS TAX REFUND

If you use Idaho

IDAHO FUELS TAX REFUND WORKSHEET.

Section V. Line 1. Enter the number of Idaho

Line 2. Enter the number of Idaho

Line 4. Multiply line 2 by line 3 for each fuel type.

FUELS TAX DUE

Section VI. Line 1. Enter the number of untaxed gallons of fuel used for a taxable purpose during the iling period in the appropriate fuel type column. Round to the nearest whole gallon.

Line 3. Multiply line 1 by line 2 for each fuel type.

USE TAX DUE

Complete Section VII to report fuel USED on or after October 1, 2006, at 6%.

SPECIFIC LINE INSTRUCTIONS FOR SECTION VII You must separately calculate and report the USE TAX

EFO00055p5

Instructions for Idaho Form 75 - page 3

DUE in Section VII if you are reporting use tax and the fuel use falls under two or more of the following situations:

•Use qualiies for a federal tax refund.

•Use does not qualify for a federal tax refund.

•You are reporting dyed diesel fuel.

Make a copy of page 2 of the Form 75 for each additional calculation. Total the USE TAX DUE from each page 2 and include in the total for Section IV, line 5 of the Form 75.

Line 1. In the appropriate fuel type column, enter the number of gallons of fuel from Section V, line 2, or the number of gallons of untaxed fuel, that do not qualify for a sales tax exemption.

Line 2. To compute the average price per gallon, irst add the total cost of fuel for each fuel type purchased during the refund period. Next, divide that total by the number of gallons on line 1 in the same column. The computation must be carried to 4 decimal places (x.xxxx).

Line 3. Do not use line 3 for dyed diesel fuel because the state fuels tax is not included in the price of dyed diesel fuel.

Line 4. Enter the federal tax rate for each fuel type if:

•You purchased fuel that included the federal tax in the price, and

•You are eligible to receive a refund of the federal tax on that fuel.

For example:

•Federal refundable use. You may use line 4 if you are a contractor who purchased undyed diesel fuel, paid the federal tax, and used the fuel in a backhoe. If you have questions about federal nontaxable uses of fuel, please contact the Internal Revenue Service (IRS).

•Federal nonrefundable use. Do not use line 4 if you use undyed diesel fuel in a registered motor vehicle for which a refund of the federal tax is not allowed.

•Dyed diesel fuel. Do not use line 4 for dyed diesel fuel because the federal fuels tax is not included in the price of dyed diesel fuel.

Note: Line 4 is for calculation purposes only. You must make federal tax refund claims to the IRS.

Federal Tax raTes (as oF 7/1/2008)

|

av |

Jet |

Undyed |

|

Com Nat |

liq Nat |

Gasoline |

Gas |

Fuel |

diesel |

Propane |

Gas |

Gas |

|

|

|

|

|

|

|

.184 |

.194 |

.219 |

.244 |

.183 |

$.183* |

.243 |

|

|

|

|

|

|

|

*Per thousand cubic feet. One thousand cubic feet equals 10 therms/gallons.

TOTAL REFUND OR TAX DUE

Section IV. Complete lines 1 through 7. (If the box for line 5 is checked, enter 0 on that line.)

If you are iling this Form 75 with your Idaho income

tax return, enter amounts from the following lines on your tax return.

•Section IV, line 1 on the Gasoline tax refund line.

•Section IV, line 2 on the Special fuels tax refund line.

•Section IV, the total of lines 3 and 4 on the Special fuels tax due line.

•Section IV, line 5 on the Sales/use tax due line.

SIGNATURE

You must sign Form 75 if you ile it separately from your income tax return. An unsigned form will delay your

refund.

Here are five common misconceptions about the Idaho 75 form:

This is not true. Any individual or entity that purchases 50 gallons or more of Idaho tax-paid gasoline or any amount of special fuels can file for a refund.

This is incorrect. Gasoline used in registered motor vehicles does not qualify for a refund under the Idaho 75 form.

This is a misunderstanding. You can file the form monthly, quarterly, annually, or for any alternate period that is more than one month but less than one year.

This is false. You must maintain records that support your claim, including receipts for tax-paid fuel purchased and details on how much was used for nontaxable purposes.

This is misleading. The form is applicable to various business activities, including logging, construction, and landscaping, among others.